Table of Content

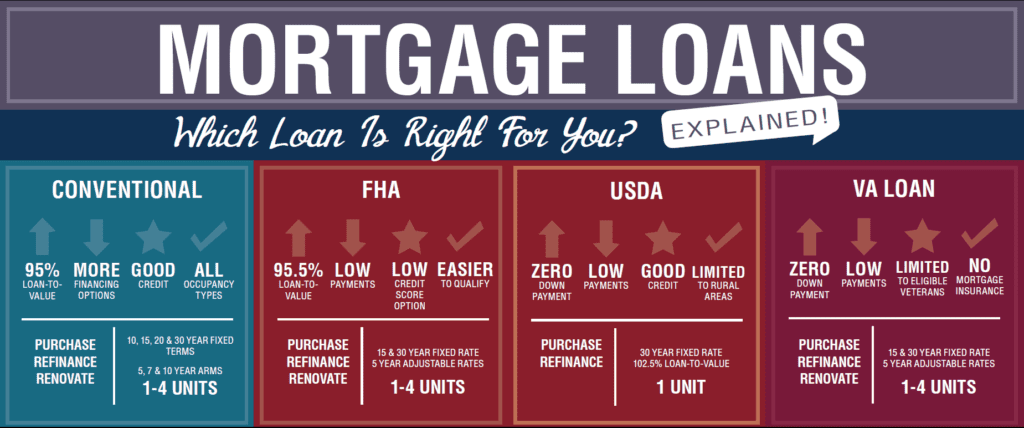

VA home loans are available for both purchase and refinance, and for first-time homebuyers and repeat homebuyers. To be eligible for a VA loan, there are a number of requirements set by the VA - A full list of those requirements can be found online on the U.S. With an FHA loan, the home must be occupied as your primary residence and meet price and property requirements, which are set by the government based on the county in which you are purchasing.

Other hybrid loans may start with a fixed interest rate for several years, and then later change to another fixed interest rate for the remainder of the loan term. While USDA loans do not have PMI, they do include what the USDA refers to as funding fees, which guarantee loan losses are paid through the fees collected rather than taxpayer funds. Veterans Administration, these home mortgages were created solely for U.S. military members and their families who meet specific criteria. They allow more military borrowers to overcome the challenges of high down payments and demanding credit requirements.

The Different Mortgage Types for Homebuyers in 2018

This is because, if your down payment is high enough, you can avoid paying PMI or other types of mortgage insurance, which can lower your monthly payments. Rates for non-conforming mortgages tend to vary more because guidelines are set by the lenders themselves or a group of investors. Loans that require excellent credit, cash reserves, and higher down payments will usually carry lower rates than riskier products. When trying to decide between the different types of home loans, you’ll realize there’s a whole new world of mortgage rates and downpayments.

The borrower’s credit score must be 640 or higher, with some exceptions. Within each type of mortgage, the length and rate type can vary. Her expertise includes mortgages, credit card rewards, and personal finance.

Know your home loans

In this mortgage, the rate will remain flat for the first five years of the loan, but after that the lender has the ability to adjust the rate annually based on current market costs. Commonly referred to as government-backed mortgages, non-conventional mortgages are guaranteed, at least in part, by a governing entity – even if a borrower defaults. Some of the most common non-conventional mortgages include FHA, VA, and USDA mortgages. For bank loans, variable rates will kick in after the fixed rate lock-in period ends . USDA mortgage – a USDA loan program, also known as the USDA Rural Development Guaranteed Housing Loan Program.

We’ll take care of the details while you take care of business. Read the terms and conditions and understand what the new package offers. Ask your bank to take you through the fact sheet so that you know what you are committing to when you take up the loan. Even if you are eligible for a bigger loan or a longer loan tenure, do not take it up unless you are sure you will have the resources to fund it. The common method of calculating interest is monthly reducing . It's also true that your first home doesn't have to be your dream home.

Property loan fact sheet

Many borrowers have gotten into financial trouble after taking out an ARM. If you pay the loan off quickly, you could pay a lot less money in interest. 3/3 and 3/1 ARMs – Similar to the 5/5 and 5/1 ARMs, except the initial fixed-rate changes after 3 years. For the 3/3 ARM, the interest rate changes every 3 years and for the 3/1 ARM, it changes every year. These limits vary by state, so you’ll need to check the FHA’s website to see what the guidelines are for your area. We will never ever recommend a product or service that we wouldn't use ourselves.

Other websites which you may navigate to from the credit union’s site are not bound by the First Service Website Privacy Policy. Purchasing a home, especially in today’s hot housing market, can be complex. That’s why many potential homebuyers prefer to work with a real estate agent. Here we look more closely at eight popular types of mortgages and compare them. Because there is so much at stake, choosing a reliable lender is crucial – especially for first-time homebuyers. It’s best to find someone who takes the time to adequately explain your options and help you understand them well.

Most Read

Plus, with so many types of home loans, it can be hard to find one that best fits your needs while still getting into the home you want. The FHA mortgage was created to expand homeownership in the US with low down payments and flexible underwriting. But FHA should not be considered the first choice just because you are a first-timer or have a small down payment. You prove your income with bank statements instead of tax returns.

The fixed-rate mortgage is one of the most standard and frequently used interest rates for home loans. It does not change based on the market; it stays the same for the entire length of the mortgage term, which is often 15 or 30 years. The fixed-rate mortgage relies on a steady concept that the homebuyer will make the same monthly payment for the duration of the loan agreement. An adjustable-rate mortgage , sometimes called a variable-rate mortgage or tracker mortgage, is a home loan that may have periodic changes to the interest rate.

For instance, the needs of a property flipper differ from a self-employed applicant who wants a forever home, or someone with credit problems but plenty of income. Federal laws require all lenders to determine your ability to repay. However, you may be able to prove your income with bank statements rather than tax returns. Others who choose non-prime financing may have good credit, but they don’t have time to waste.

There are occasions where a homebuyer might select a balloon mortgage because they don’t expect to stay in their home very long. However, they would not build equity in the home and may not be better off than if they had rented. Your next adventure awaits you Whether you’re purchasing a new or used vehicle or simply looking to refinance your current vehicle, First Service can help you explore your new adventure with ease. The advertised rates and effective interest rate for the packages. The updated repayment schedules for the various packages – check the interest payable. To find out if you are eligible for an HDB loan and the maximum amount you can borrow, you will need to apply for an HDB Loan Eligibility letter.

No comments:

Post a Comment